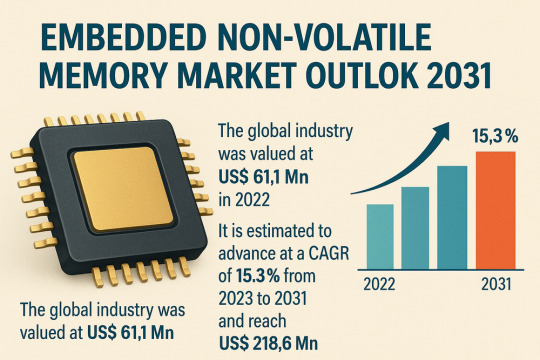

#Embedded Processor Market Report

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr has 16.74 million mobile monthly users in the US.

Text

Environmental Monitoring Devices Go Ultra-Sensitive with Nano Light

The global nanophotonics market, valued at USD 25.6 billion in 2023 and projected to surpass USD 45 billion by 2031 at a CAGR of 7.9%, is witnessing robust growth driven by rising innovation in telecommunications and increasing R&D investments, particularly in North America. Nanophotonics enables manipulation of light at the nanoscale, revolutionizing applications in optoelectronics, displays, and biomedical imaging. Market competition is intensifying with key players like EPISTAR Corporation, Samsung SDI Co Ltd., and OSRAM Licht AG expanding their technological capabilities to capture emerging opportunities across industries.

Unlock exclusive insights with our detailed sample report :

Key Market Drivers

1. Growing Demand for Faster, Low-Energy Data Transmission

With explosive data generation, data centers and cloud systems demand ultra-fast, energy-efficient data transfer. Nanophotonic components like photonic integrated circuits (PICs) are revolutionizing how data is moved, processed, and stored.

2. Surge in LED and OLED Technologies

Widespread adoption of LED and OLED displays in televisions, smartphones, automotive dashboards, and wearable tech has significantly increased the demand for nanophotonic light emitters and filters, especially those based on quantum dots and plasmonics.

3. Advancements in Photonic Chips for AI and Machine Learning

AI and high-performance computing are integrating nanophotonic optical interconnects into chips to minimize latency and heat, improving processing speeds while reducing energy consumption.

4. Quantum Computing and Security Applications

Nanophotonics is fundamental to quantum communication and cryptography, enabling high-speed, unbreakable data transmission protocols through single-photon sources and waveguides.

5. Rising Applications in Biophotonics and Healthcare

Non-invasive medical diagnostics, biosensors, and real-time imaging are leveraging nanophotonic sensors to achieve superior sensitivity, resolution, and accuracy, especially in cancer detection and genomic sequencing.

Regional Trends

United States

The U.S. nanophotonics market benefits from:

Robust semiconductor policy investments such as the CHIPS Act.

Heavy investments by firms like Intel, NVIDIA, and IBM in optical computing, including photonics-powered AI accelerators.

Collaborations with universities like MIT and Stanford, advancing research in light-based transistors, plasmonic circuits, and meta-optics.

Expansion into military-grade nanophotonics, especially for secure communication and space-grade sensors.

Japan

Japan remains a global leader in:

Miniaturized optics for automotive lidar, biomedical tools, and AR/VR headsets.

Integration of nanophotonics into robotics and factory automation, essential to Industry 5.0.

Development of compact biosensors using metallic nanostructures and quantum dots for use in home diagnostics and elderly care.

Notable progress is being made by companies such as Hamamatsu Photonics, Panasonic, and Sony, in collaboration with R&D institutes like RIKEN and NIMS.

Speak to Our Senior Analyst and Get Customization in the report as per your requirements:

Industry Segmentation

By Product:

Light-Emitting Diodes (LEDs)

Organic LEDs (OLEDs)

Photonic Integrated Circuits (PICs)

Optical Switches

Solar Photovoltaic Devices

Laser Diodes

Near-field Optical Components

By Material:

Plasmonic Nanostructures

Photonic Crystals

Semiconductor Quantum Dots

Carbon Nanotubes

Nanowires

By Application:

Consumer Electronics

Telecommunications

Healthcare & Life Sciences

Defense & Aerospace

Energy and Solar Cells

Automotive & Smart Mobility

Latest Industry Trends

AI Chips Powered by Nanophotonics U.S. startups are integrating light-based transistors into neural processors, enabling ultrafast computation with reduced energy overhead.

Next-Gen Displays with Quantum Dot Emitters Quantum dots embedded in nanophotonic architectures improve brightness, color fidelity, and efficiency in displays across smartphones and TVs.

Photonic Neural Networks in Development Light-based neural nets are being tested in Japan and the U.S. to replace electrical interconnects in deep learning hardware.

Nanophotonic Biosensors for Real-Time Diagnostics Portable nanophotonic devices for glucose monitoring, cancer markers, and airborne pathogen detection are gaining traction post-pandemic.

Flexible and Wearable Nanophotonic Devices Researchers are developing bendable and transparent photonic circuits for integration into smart textiles and wearable health trackers.

Buy the exclusive full report here:

Growth Opportunities

Data Center Optics: Expanding demand for optical interconnects in hyperscale data centers.

Automotive LiDAR and Optical Sensors: Nanophotonic lidar solutions are being miniaturized for next-gen autonomous driving.

Healthcare and Point-of-Care Devices: Growing use of on-chip diagnostic tools in both clinical and at-home settings.

5G & Beyond: Nanophotonics supports the backbone of high-speed network infrastructure with integrated optical circuits.

Space and Defense: Lightweight, ultra-sensitive nanophotonic sensors for space exploration, drones, and military surveillance.

Competitive Landscape

Major players in the global nanophotonics market include:

Intel Corporation

NKT Photonics

Hamamatsu Photonics

Samsung Electronics

Mellanox Technologies (NVIDIA)

Sony Corporation

Osram Licht AG

Luxtera (Cisco)

IBM Corporation

Mellanox Technologies

These companies are investing in:

Photonics foundries and wafer-level integration.

Startups and university spin-offs focused on next-gen light control and biosensing.

Joint ventures for scaling quantum and optical chip production.

Stay informed with the latest industry insights-start your subscription now:

Conclusion

The nanophotonics market is emerging as a pivotal enabler across a wide spectrum of industries—from semiconductors and smart electronics to biotech and energy systems. As global demand intensifies for faster data transmission, energy efficiency, and miniaturization, nanophotonics offers scalable, sustainable solutions.

With leading countries like the United States and Japan investing heavily in R&D, infrastructure, and commercialization strategies, the market is entering a phase of high-value growth and disruption. The convergence of nanotechnology, AI, and photonics is shaping a future defined by faster, smarter, and more resilient technologies.

About us:

DataM Intelligence is a premier provider of market research and consulting services, offering a full spectrum of business intelligence solutions—from foundational research to strategic consulting. We utilize proprietary trends, insights, and developments to equip our clients with fast, informed, and effective decision-making tools.

Our research repository comprises more than 6,300 detailed reports covering over 40 industries, serving the evolving research demands of 200+ companies in 50+ countries. Whether through syndicated studies or customized research, our robust methodologies ensure precise, actionable intelligence tailored to your business landscape.

Contact US:

Company Name: DataM Intelligence

Contact Person: Sai Kiran

Email: [email protected]

Phone: +1 877 441 4866

Website: https://www.datamintelligence.com

#Nanophotonics market#Nanophotonics market size#Nanophotonics market growth#Nanophotonics market share#Nanophotonics market analysis

0 notes

Text

PICMG Single Board Computer Market: Growth Fueled by Energy Efficiency Demand

MARKET INSIGHTS

The global PICMG Single Board Computer Market size was valued at US$ 678.4 million in 2024 and is projected to reach US$ 1,180 million by 2032, at a CAGR of 8.35% during the forecast period 2025-2032. The U.S. market accounts for approximately 32% of global revenue, while China is expected to witness the fastest growth at 12.3% CAGR through 2032.

PICMG (PCI Industrial Computer Manufacturers Group) Single Board Computers are ruggedized embedded computing solutions designed for industrial applications. These standardized boards integrate processors, memory, and I/O interfaces on a single PCB, conforming to PICMG specifications for reliability in harsh environments. The technology includes two primary form factors: PICMG Half-size (reduced footprint) and PICMG Full-size (extended functionality) architectures.

The market growth is driven by increasing automation across industries, rising demand for edge computing solutions, and stringent requirements for military-grade electronics. Recent advancements in industrial IoT and 5G infrastructure are creating new opportunities, particularly in smart manufacturing and autonomous systems. Key players like Advantech and ADLINK collectively hold over 45% market share, with recent product launches featuring Intel’s 13th Gen processors and enhanced thermal management solutions for extreme environments.

MARKET DRIVERS

Rising Demand for Rugged Embedded Solutions Accelerates PICMG SBC Adoption

The industrial sector’s increasing need for reliable computing systems in harsh environments is driving widespread adoption of PICMG single board computers. These modular systems offer superior thermal tolerance, shock resistance, and extended lifecycle support compared to commercial-grade alternatives. Across energy infrastructure, manufacturing floors, and transportation systems, PICMG SBCs demonstrate operational reliability with mean time between failures exceeding 100,000 hours in temperature ranges from -40°C to 85°C. This durability translates to reduced downtime and maintenance costs, making them indispensable for mission-critical applications.

Military Modernization Programs Fuel Defense Sector Growth

Global defense spending exceeding $2 trillion annually underscores substantial opportunities for PICMG-based computing solutions. Military applications demand strict compliance with standards like MIL-STD-810G for environmental durability and MIL-STD-461 for electromagnetic compatibility. The modular architecture of PICMG SBCs enables seamless integration with legacy systems while providing the computational power needed for modern battlefield networks, radar processing, and electronic warfare systems. Recent contracts for next-generation armored vehicles and unmanned systems frequently specify PICMG architectures due to their proven reliability in theater operations.

Industry 4.0 Transition Demands Edge Computing Capabilities

The fourth industrial revolution is driving unprecedented demand for industrial-grade edge computing solutions. PICMG SBCs bridge the gap between operational technology and information technology with their modular expandability and deterministic performance. Manufacturers implementing smart factory initiatives report 30-50% improvements in production efficiency when deploying PICMG-based solutions for real-time process control and predictive maintenance. Standardization across the PICMG ecosystem ensures compatibility with industrial protocols like PROFINET, EtherCAT, and OPC UA, significantly reducing integration complexity in brownfield deployments.

MARKET RESTRAINTS

High Initial Costs Limit Adoption in Price-Sensitive Markets

While PICMG SBCs offer exceptional long-term value, their upfront costs present a significant hurdle for budget-constrained organizations. Commercial off-the-shelf alternatives often appear attractive at 30-50% lower initial price points, despite lacking industrial-grade reliability certifications. This cost differential proves particularly challenging in emerging markets where project financing prioritizes short-term capital expenditure over lifecycle costs. Furthermore, the specialized components and rigorous testing required for industrial certification contribute to longer lead times, sometimes exceeding 16 weeks for customized configurations.

System Integration Complexity Deters Smaller Enterprises

The technical sophistication required to implement PICMG-based solutions creates barriers for organizations lacking specialized IT/OT integration teams. Unlike turnkey industrial PCs, modular PICMG systems demand careful consideration of backplane compatibility, power requirements, and thermal management. Surveys indicate nearly 40% of first-time adopters experience delays during implementation due to unforeseen integration challenges. This complexity often pushes small and medium enterprises toward less robust but more plug-and-play alternatives, despite the long-term operational advantages of PICMG architectures.

MARKET CHALLENGES

Component Shortages Disrupt Supply Chain Reliability

The industrial electronics sector continues grappling with procurement challenges for critical semiconductors and passive components. PICMG SBC manufacturers face particular difficulties sourcing military-grade FPGAs and extended temperature range memory modules, with lead times for some components stretching beyond 52 weeks. This supply chain volatility forces difficult trade-offs between design flexibility and component availability. Several leading vendors have reported inventory carrying costs increasing by 25-35% as they attempt to buffer against unpredictable supply disruptions.

Competition from Compact Form Factors Intensifies

Emerging embedded standards like SMARC and Qseven present competitive challenges to traditional PICMG architectures in space-constrained applications. These compact modules offer similar industrial certifications in packages up to 80% smaller than full-size PICMG boards. While they lack the expansion capabilities of PICMG systems, their reduced footprint proves advantageous in mobile robotics, UAVs, and wearable military systems. Market data suggests compact form factors are gaining 3-5% market share annually in applications where size and weight outweigh expansion requirements.

MARKET OPPORTUNITIES

5G Network Rollouts Create New Edge Deployment Scenarios

The global 5G infrastructure buildout presents transformative opportunities for PICMG-based edge computing solutions. Telecom operators require ruggedized computing platforms at cell sites to support Open RAN architectures and network function virtualization. PICMG SBCs perfectly match these requirements with their modular design, enabling field-upgradable processing capacity. Early deployments in 5G macro and small cell installations demonstrate 60-70% reductions in maintenance visits compared to conventional telecom servers, driving strong interest from network equipment providers.

Artificial Intelligence at the Edge Expands Addressable Market

The exponential growth of edge AI applications creates substantial opportunities for PICMG platforms combining deterministic real-time processing with neural network acceleration. Modern PICMG SBCs now integrate dedicated AI processors capable of 35 TOPS while maintaining industrial operating specifications. This enables new use cases in autonomous systems, predictive maintenance, and real-time quality inspection—markets projected to grow at 28% CAGR through 2030. The modular nature of PICMG systems allows enterprises to scale AI capabilities across their operations without complete system replacements.

Growing Emphasis on Cybersecurity Opens New Verticals

Increasing cybersecurity regulations for critical infrastructure are driving demand for secure-by-design computing platforms. PICMG SBCs incorporate hardware-rooted security features including TPM 2.0, secure boot, and hardware crypto acceleration—capabilities now mandated in sectors like energy transmission and water management. Recent specifications for PICMG 1.3 add enhanced security provisions, making these systems particularly attractive for government and utility applications. Market analysts note a 40% increase in security-focused procurements specifying PICMG architectures over the past two years.

PICMG SINGLE BOARD COMPUTER MARKET TRENDS

Industrial Automation and Edge Computing Driving Market Growth

The PICMG single board computer market is experiencing steady growth, primarily fueled by the increasing adoption of industrial automation and edge computing solutions. These compact yet powerful boards are becoming indispensable in manufacturing environments where reliability and real-time processing are critical. Recent data indicates that edge computing deployments in industrial settings are expected to grow at a compound annual growth rate (CAGR) of over 20% through 2030, directly benefiting PICMG-compliant solutions. Furthermore, the integration of AI-enabled processing at the edge is accelerating demand for high-performance single board computers that comply with PICMG standards for ruggedness and modular architecture.

Other Trends

Military and Aerospace Applications

The defense sector represents one of the most significant growth avenues for PICMG single board computers, driven by stringent requirements for secure, high-availability computing in harsh environments. Modern military communications systems, unmanned platforms, and avionics increasingly rely on PICMG 1.3 and 2.16 compliant solutions for their proven interoperability and extended lifecycle support. While commercial sectors might prioritize cost reductions, defense applications focus on radiation-hardened designs and extended temperature ranges, creating specialized market niches with higher margins for manufacturers.

Transition to PCIe-Based Architectures

A fundamental technological shift occurring in the PICMG ecosystem involves the migration from legacy PCI/ISA architectures to modern PCI Express-based systems. This transition is particularly evident in the growing preference for PICMG 1.3 over older 1.0 standards, as it supports higher bandwidth interfaces critical for contemporary applications. Market analysis suggests that PCIe-enabled PICMG boards now account for approximately 65% of new deployments, with this percentage expected to exceed 85% by 2028. The change reflects broader industry demands for enhanced I/O capabilities to support high-speed data acquisition, machine vision systems, and 5G infrastructure components.

The PICMG market evolution also shows interesting regional variations. While North America and Europe maintain strong positions in innovation and high-performance applications, Asia-Pacific demonstrates the fastest growth trajectory, particularly in industrial automation deployments. This geographical diversification presents both opportunities and challenges for manufacturers striving to balance standardization with regional technical requirements and certification mandates.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Define Market Competition in PICMG SBC Sector

The PICMG Single Board Computer market exhibits a moderately consolidated structure, with leading players holding approximately 45-50% of the global market share in 2024. Advantech emerges as the dominant force, leveraging its comprehensive product portfolio and robust manufacturing capabilities across Taiwan, China, and North America. The company’s recent introduction of the AIMB-218 industrial motherboard demonstrates its commitment to innovation in rugged computing solutions.

Axiomtek and ADLINK Technology follow closely, capturing significant market traction through their specialization in industrial-grade solutions for harsh environments. Both companies have demonstrated consistent growth through strategic acquisitions and partnerships – Axiomtek’s expansion into AIoT applications and ADLINK’s focus on edge computing solutions position them strongly in the data center and industrial automation segments.

Market consolidation continues apace, with mid-tier players pursuing aggressive R&D strategies to differentiate their offerings. Taiwanese manufacturers IEI Integration and ASUS maintain strong positions through vertical integration and cost-efficient production models, particularly in the Asia-Pacific region where demand for PICMG-compliant solutions grows steadily.

Meanwhile, emerging players like Broadax Systems and ICP America are gaining traction through specialization in niche applications such as military communications and energy sector automation. These companies focus on delivering customized solutions with extended lifecycle support – a critical requirement in defense and infrastructure applications.

List of Key PICMG Single Board Computer Manufacturers

Advantech Co., Ltd. (Taiwan)

Axiomtek Co., Ltd. (Taiwan)

ADLINK Technology (Taiwan)

IEI Integration Corp. (Taiwan)

ASUS (Taiwan)

Portwell, Inc. (U.S.)

ICP America, Inc. (U.S.)

Broadax Systems, Inc. (U.S.)

AAEON Technology (Taiwan)

IBASE Technology (Taiwan)

COMMELL (Taiwan)

NEXCOM International (Taiwan)

PICMG Single Board Computer Market

Segment Analysis:

By Type

PICMG Half-size Single Board Computer Segment Leads Due to Compact Design and Cost Efficiency

The market is segmented based on type into:

PICMG Half-size Single Board Computer

PICMG Full-size Single Board Computer

By Application

Data Centers Segment Dominates With High Demand for Edge Computing Solutions

The market is segmented based on application into:

Energy and Power

Data Centers

Military and Aerospace

Education and Research

General Industrial

Others

By End User

Industrial Automation Sector Holds Significant Market Share

The market is segmented based on end user into:

Manufacturing Industries

IT and Telecommunications

Government and Defense

Healthcare

Others

Regional Analysis: PICMG Single Board Computer Market

North America North America remains a strategic market for PICMG single-board computers, driven by strong demand from defense, industrial automation, and data center applications. The region benefits from high R&D investments and early adoption of embedded computing technologies. The U.S. dominates with a significant market share, supported by thriving semiconductor innovation and governmental funding in defense modernization programs. Canada and Mexico also show steady growth, particularly in manufacturing automation. Challenges include supply chain complexities and rising component costs, but vendors like Advantech and AAEON maintain strong footholds by offering ruggedized solutions for harsh industrial environments.

Europe Europe showcases robust demand for PICMG-compliant SBCs, particularly in Germany, France, and the U.K., where industrial automation and smart manufacturing initiatives are accelerating. The region emphasizes energy-efficient designs and compliance with EU RoHS directives, pushing manufacturers to innovate towards lower power consumption. Germany leads in adoption for machine vision and Industry 4.0 applications. However, slower economic growth in some countries tempers market expansion. Local players like ADLINK capitalize on the need for high-reliability systems in medical and transportation sectors, where long product lifecycles are critical.

Asia-Pacific As the fastest-growing region, Asia-Pacific thrives on manufacturing hubs in China, Japan, and South Korea. China alone accounts for over 35% of global production, with heavy usage in telecommunications and energy infrastructure. India emerges as a key growth market with rising investments in digital infrastructure. Japan retains dominance in precision industrial applications, while Southeast Asian nations show increasing demand for cost-effective automation solutions. Pricing pressures from local competitors like ASUS and IEI Integration drive innovation, though IP protection concerns persist. Taiwan serves as a major production base for global vendors.

South America Market maturity varies significantly across South America, where Brazil and Argentina lead in deploying PICMG SBCs for oil & gas monitoring and agricultural automation. Growth is hindered by economic instability, currency fluctuations, and reliance on imports. Nonetheless, modernization of manufacturing facilities and gradual adoption of IoT technologies create opportunities. Local partnerships with international brands like Axiomtek help address customization needs for mining and renewable energy applications. Infrastructure limitations in rural areas slow broader adoption compared to other regions.

Middle East & Africa This region presents high-potential niche opportunities, particularly in oil-rich GCC nations investing in smart city projects and digital transformation. Israel stands out for military and aerospace applications requiring secure embedded systems. South Africa shows growing uptake in mining automation. However, the market remains price-sensitive, with slower adoption rates due to limited local technical expertise and reliance on foreign suppliers. Dubai’s focus on becoming a tech hub drives data center investments, benefiting suppliers of high-availability PICMG solutions. Long sales cycles and geopolitical risks challenge faster expansion.

Report Scope

This market research report provides a comprehensive analysis of the global and regional PICMG Single Board Computer markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Related Reports:https://semiconductorblogs21.blogspot.com/2025/06/laser-diode-cover-glass-market-valued.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/q-switches-for-industrial-market-key.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/ntc-smd-thermistor-market-emerging_19.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/lightning-rod-for-building-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/cpe-chip-market-analysis-cagr-of-121.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/line-array-detector-market-key-players.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/tape-heaters-market-industry-size-share.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/wavelength-division-multiplexing-module.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/electronic-spacer-market-report.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/5g-iot-chip-market-technology-trends.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/polarization-beam-combiner-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/amorphous-selenium-detector-market-key.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/output-mode-cleaners-market-industry.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/digitally-controlled-attenuators-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/thin-double-sided-fpc-market-key.html

0 notes

Text

IoT Chips Market is Driven by Explosive Connectivity Demand

Internet of Things (IoT) chips are specialized microprocessors, system-on-chips (SoCs), and connectivity modules designed to enable seamless data exchange among sensors, devices, and cloud platforms. These chips incorporate ultra-low-power architectures, embedded security protocols, and advanced signal processing capabilities that support a broad spectrum of IoT applications—from smart homes and wearable gadgets to industrial automation and connected vehicles. Advantages include reduced latency through edge computing, optimized energy efficiency for battery-operated devices, and streamlined integration into existing network infrastructures.

As businesses pursue digital transformation, there is a growing need for reliable, scalable chipsets capable of handling massive device connectivity, real-time analytics, and robust encryption. Continuous innovation in semiconductor fabrication processes has driven down production costs and boosted performance metrics, enabling smaller startups and established market players alike to introduce competitive products. Meanwhile, evolving market trends such as 5G rollout, AI-enabled analytics, and smart city initiatives are creating new IoT Chips Market opportunities and shaping the industry landscape. Comprehensive market research highlights expanding market segments in healthcare monitoring, agricultural sensors, and asset tracking.

The IoT chips market is estimated to be valued at USD 620.36 Bn in 2025 and is expected to reach USD 1415.005 Bn by 2032, growing at a compound annual growth rate (CAGR) of 15.00% from 2025 to 2032. Key Takeaways

Key players operating in the IoT Chips Market are:

-Intel Corporation

-Samsung Electronics Co. Ltd

-Qualcomm Technologies Inc.

-Texas Instruments Incorporated

-NXP Semiconductors NV

These market companies have established strong footholds through diversified product portfolios that span microcontrollers, application processors, short-range wireless SoCs, and AI inference engines. Their strategic investments in R&D, partnerships with tier-one automotive and industrial firms, and capacity expansions in fabrication plants are instrumental in driving market share growth. Robust alliances and licensing agreements help these players accelerate time-to-market for next-generation solutions, while continuous performance enhancements maintain their competitive edge. As major players optimize supply chains and strengthen IP portfolios, they contribute significantly to the overall market dynamics and industry size. The growing demand for IoT chips is fueled by accelerated digitalization across verticals such as automotive, healthcare, consumer electronics, and manufacturing. Automotive OEMs are integrating IoT chips for connected car features—remote diagnostics, vehicle-to-everything (V2X) communication, and advanced driver-assistance systems (ADAS)—driving substantial market growth. In healthcare, remote patient monitoring and telemedicine solutions rely on miniaturized, power-efficient chips to ensure continuous data transmission and secure access. Additionally, smart agriculture applications leverage low-cost sensors and communication modules to optimize resource usage and crop yields. As enterprises embrace Industry 4.0, the deployment of IoT solutions for predictive maintenance and asset tracking has become a critical business growth strategy. These evolving market trends underscore the importance of high-performance, cost-effective IoT chips to sustain long-term expansion.

‣ Get More Insights On: IoT Chips Market

‣ Get this Report in Japanese Language: IoTチップ市場

‣ Get this Report in Korean Language: IoT칩시장

0 notes

Text

How do self-healing protocols enhance IoT device longevity in harsh environments

TheIoT Communication Protocol Market Size was valued at USD 16.95 Billion in 2023 and is expected to reach USD 23.94 Billion by 2032 and grow at a CAGR of 4.2% over the forecast period 2024-2032.

The IoT Communication Protocol Market is experiencing unprecedented growth, driven by the pervasive integration of connected devices across industries. This market is crucial for enabling the seamless exchange of data between the billions of IoT devices, from smart home appliances to complex industrial sensors, forming the backbone of our increasingly interconnected world. The evolution of communication protocols is vital to unlock the full potential of the Internet of Things, ensuring efficiency, security, and scalability in every deployment.

U.S. Headline: IoT Communication Protocol Market Poised for Significant Expansion Driven by Smart Infrastructure Demands

IoT Communication Protocol Market continues its robust expansion, fueled by advancements in wireless technologies and the rising demand for real-time data exchange. As the Internet of Things ecosystem matures, the emphasis on interoperability, low-power consumption, and enhanced security features in communication protocols becomes paramount. This dynamic landscape necessitates continuous innovation to support the diverse and expanding array of IoT applications that are reshaping industries globally.

Get Sample Copy of This Report: https://www.snsinsider.com/sample-request/6554

Market Keyplayers:

Huawei Technologies (OceanConnect IoT Platform, LiteOS)

Arm Holdings (Mbed OS, Cortex‑M33 Processor)

Texas Instruments (SimpleLink CC3220 Wi‑Fi MCU, SimpleLink CC2652 Multiprotocol Wireless MCU)

Intel (XMM 7115 NB‑IoT Modem, XMM 7315 LTE‑M/NB‑IoT Modem)

Cisco Systems (Catalyst IR1101 Rugged Router, IoT Control Center)

NXP Semiconductors (LPC55S6x Cortex‑M33 MCU, EdgeLock SE050 Secure Element)

STMicroelectronics (STM32WL5x LoRaWAN Wireless MCU, SPIRIT1 Sub‑GHz Transceiver)

Thales (Cinterion TX62 LTE‑M/NB‑IoT Module, Cinterion ENS22 NB‑IoT Module)

Zebra Technologies (Savanna IoT Platform, SmartLens for Retail Asset Visibility)

Wind River (Helix Virtualization Platform, Helix Device Cloud)

Ericsson (IoT Accelerator, Connected Vehicle Cloud)

Qualcomm (IoT Services Suite, AllJoyn Framework)

Samsung Electronics (ARTIK Secure IoT Modules, SmartThings Cloud)

IBM (Watson IoT Platform, Watson IoT Message Gateway)

Market Analysis

The IoT Communication Protocol Market is on a clear upward trajectory, reflecting the global acceleration in IoT device adoption across consumer electronics, industrial automation, healthcare, and smart city initiatives. This growth is intrinsically linked to the demand for efficient, reliable, and secure data transmission. Key drivers include the proliferation of 5G networks, the imperative for edge computing, and the integration of AI for smarter decision-making, all of which heavily rely on robust communication foundations. The market is witnessing a strong shift towards wireless and low-power consumption technologies, with standardized protocols becoming increasingly critical for widespread interoperability.

Market Trends

Proliferation of Wireless Technologies: A dominant shift towards wireless protocols like Wi-Fi, Bluetooth, Zigbee, LoRaWAN, and NB-IoT, preferred for their flexibility and ease of deployment.

5G Integration: The rollout of 5G networks is revolutionizing IoT communication, offering unprecedented speeds, ultra-low latency, and enhanced capacity for real-time applications such, as autonomous vehicles and advanced telemedicine.

Edge Computing Synergy: Growing integration of edge computing with IoT protocols to process data closer to the source, significantly reducing latency and bandwidth consumption, crucial for time-sensitive applications.

Enhanced Security Protocols: A paramount focus on embedding advanced encryption, authentication, and data integrity layers within communication protocols to combat escalating cyber threats and ensure data privacy.

Standardization and Interoperability: A strong industry-wide push for unified communication frameworks to ensure seamless interaction between devices from diverse manufacturers, minimizing vendor lock-in and fostering a more cohesive IoT ecosystem.

AI-Enabled Communications: Increasing integration of Artificial Intelligence into IoT protocols to facilitate smarter decision-making, predictive analytics, and automated optimization of communication pathways.

Market Scope

The IoT Communication Protocol Market's reach is expansive, touching virtually every sector:

Smart Homes & Consumer Electronics: Enabling seamless connectivity for intelligent appliances, smart lighting, voice assistants, and wearables.

Industrial IoT (IIoT) & Manufacturing: Facilitating real-time monitoring, predictive maintenance, and operational efficiency in factories and industrial settings.

Healthcare: Powering remote patient monitoring, connected medical devices, and smart hospital infrastructure for improved patient care and operational insights.

Smart Cities & Utilities: Supporting intelligent traffic management, energy grids, environmental monitoring, and public safety applications.

Automotive & Transportation: Crucial for connected vehicles, intelligent transportation systems, and fleet management, enhancing safety and efficiency.

Agriculture: Enabling precision farming through sensor data for optimized irrigation, crop monitoring, and livestock management.

Forecast Outlook

The future of the IoT Communication Protocol Market appears incredibly promising, driven by relentless innovation and an ever-increasing global demand for connected solutions. Anticipate a landscape characterized by increasingly sophisticated protocols, designed for superior efficiency and adaptive intelligence. The convergence of emerging technologies, such as advanced AI and ubiquitous 5G connectivity, will further accelerate the market's trajectory, fostering an era of truly pervasive and intelligent IoT deployments across all verticals. Expect a future where communication is not just about connectivity, but about seamless, secure, and context-aware interactions that redefine possibility.

Access Complete Report: https://www.snsinsider.com/reports/iot-communication-protocol-market-6554

Conclusion

As we stand on the cusp of an even more interconnected era, the IoT Communication Protocol Market is not merely a segment of the tech industry; it is the fundamental enabler of digital transformation. For innovators, developers, and enterprises alike, understanding and leveraging the evolution of these protocols is critical to building the next generation of smart solutions. This market represents an unparalleled opportunity to shape a future where every device contributes to a smarter, safer, and more efficient world. Embrace these advancements, and together, we can unlock the full, transformative power of the Internet of Things.

Related reports:

U.S.A accelerates smart agriculture adoption to boost crop efficiency and sustainability.

U.S.A. IoT MVNO market: surging demand for cost-effective, scalable connectivity

About Us:

SNS Insider is one of the leading market research and consulting agencies that dominates the market research industry globally. Our company's aim is to give clients the knowledge they require in order to function in changing circumstances. In order to give you current, accurate market data, consumer insights, and opinions so that you can make decisions with confidence, we employ a variety of techniques, including surveys, video talks, and focus groups around the world.

Contact Us:

Jagney Dave - Vice President of Client Engagement

Phone: +1-315 636 4242 (US) | +44- 20 3290 5010 (UK)

Contact Us:

Jagney Dave - Vice President of Client Engagement

Phone: +1-315 636 4242 (US) | +44- 20 3290 5010 (UK)

Mail us: [email protected]

0 notes

Text

Mobile SoC Market Expansion Strategies and Growth Opportunities to 2033

Introduction

System-on-Chip (SoC) technology has fundamentally transformed the way modern smartphones and mobile devices are designed. By integrating all critical computing components—including CPUs, GPUs, modems, AI processors, and other subsystems—onto a single chip, Mobile SoCs have enabled sleeker, more powerful, and energy-efficient devices.

As 5G networks, artificial intelligence, augmented reality, and edge computing become central to mobile computing, the global Mobile SoC market is set for significant growth. This article explores the market’s key trends, drivers, challenges, segmentation, and growth forecast through 2032.

Market Overview

The global Mobile SoC market was valued at approximately USD 115 billion in 2023 and is projected to reach USD 240 billion by 2032, growing at a CAGR of around 8.4% during the forecast period.

The market’s growth is fueled by:

The rapid adoption of 5G smartphones,

Increasing integration of artificial intelligence (AI) capabilities at the edge,

A growing demand for power-efficient chips, and

The rise of IoT-connected devices that rely on Mobile SoCs for performance.

Download a Free Sample Report:-https://tinyurl.com/yjhyn3va

Key Market Drivers

Proliferation of 5G Connectivity

The global rollout of 5G networks has led to unprecedented demand for advanced SoCs capable of handling higher data rates and supporting multiple antennas through integrated 5G modems. SoCs with 5G support are becoming a baseline requirement for smartphone manufacturers aiming to remain competitive.

Rising Demand for Edge AI and On-Device Processing

AI-driven features such as voice assistants, computational photography, facial recognition, and real-time language translation rely heavily on on-device processing. This has led to the emergence of AI accelerators embedded directly into SoCs, such as Apple’s Neural Engine or Qualcomm’s Hexagon DSP, creating a strong demand for smarter, AI-ready chips.

Increased Adoption of IoT and Wearables

Mobile SoCs aren’t limited to smartphones anymore. Devices like smartwatches, AR/VR headsets, wireless earbuds, and health trackers all leverage SoC architectures to deliver efficient performance in compact form factors. This diversification is expanding the market beyond mobile phones.

Performance and Power Efficiency Improvements

Consumers expect high performance and longer battery life. Manufacturers are racing to develop SoCs with lower process nodes (currently at 3nm and heading toward 2nm) to deliver more transistors per square millimeter while reducing power consumption.

Market Challenges

High Design Complexity and R&D Costs

The design and verification of cutting-edge Mobile SoCs are increasingly complex, requiring substantial R&D investment, sophisticated simulation tools, and long development cycles. Only a few players like Qualcomm, Apple, Samsung, and MediaTek can afford to remain at the cutting edge.

Supply Chain Vulnerabilities

The semiconductor industry has faced significant disruptions, especially in light of the COVID-19 pandemic and geopolitical tensions affecting Taiwan’s foundries (TSMC) and China’s tech manufacturing base. This can limit supply and delay the production of next-generation SoCs.

Thermal Management Issues

As SoCs pack more cores, modems, GPUs, and AI accelerators into smaller dies, heat generation has become a design bottleneck, especially for high-performance phones and compact devices.

Market Segmentation

By Type

Application Processors Responsible for running the device’s OS and apps.

Baseband Processors Handle mobile communication protocols (3G/4G/5G).

AI Accelerators Dedicated cores for machine learning inference and real-time decision-making.

Connectivity SoCs Support Wi-Fi, Bluetooth, GPS, and cellular connectivity.

By Application

Smartphones

Tablets

Wearable Devices

Automotive Infotainment Systems

Smart Home Devices

AR/VR Headsets

IoT and Edge Devices

By Region

North America Driven by strong demand for high-end devices and early 5G adoption.

Europe Growing emphasis on data security and AI-enhanced smartphones.

Asia-Pacific The largest manufacturing hub and consumer market for smartphones, especially in China, India, South Korea, and Japan.

Middle East & Africa Rising mobile penetration rates and increasing adoption of 4G/5G networks.

Latin America A fast-growing market segment with budget smartphones and IoT device demand.

Technological Trends

Smaller Process Nodes

The ongoing shift to 3nm and 2nm semiconductor technology enables faster performance and lower energy consumption. Companies like TSMC and Samsung Foundry are leading this transition.

Heterogeneous Computing

Modern SoCs combine CPUs, GPUs, Neural Processing Units (NPUs), and Digital Signal Processors (DSPs) to distribute workloads efficiently, offering better performance for AI and AR applications.

Chiplet Design

Instead of building a single monolithic die, manufacturers are exploring chiplet-based architectures, allowing them to mix and match processing units, connectivity blocks, and AI accelerators more flexibly.

Open-Source Architectures

The rise of RISC-V as a viable alternative to ARM’s proprietary cores is beginning to reshape the SoC design landscape, offering cost-effective, customizable solutions.

Competitive Landscape

The Mobile SoC market is a battleground for a few dominant players, each striving to push the boundaries of performance, efficiency, and AI capability.

Key Companies

Qualcomm Technologies Inc. — Snapdragon series

Apple Inc. — A-series and M-series SoCs

Samsung Electronics — Exynos series

MediaTek Inc. — Dimensity and Helio series

HiSilicon (Huawei) — Kirin series (limited by trade restrictions)

UNISOC — Expanding footprint in entry-level smartphones

Google — Tensor SoCs for Pixel devices

Future Outlook

The future of the Mobile SoC market will be shaped by the convergence of AI, 5G/6G, and edge computing. Here are a few trends to watch as the market matures:

On-device AI capabilities will become standard, making cloud dependence optional for complex tasks like real-time video enhancement and augmented reality overlays.

Energy optimization will become a defining feature as mobile devices increasingly rely on AI for everything from photography to app optimization.

Vertical integration (like Apple’s in-house chip design for iPhones) will increase, as tech giants aim for tighter control over performance, security, and power efficiency.

Open-source architectures and emerging fabrication techniques (e.g., extreme ultraviolet lithography) will lower barriers for new entrants and foster more innovation.

Conclusion

The Mobile SoC market stands at the crossroads of multiple technological revolutions: the rollout of 5G/6G networks, the proliferation of edge AI, and the emergence of smart and autonomous devices across industries. Despite facing headwinds like supply chain fragility and design complexity, the sector is set for long-term expansion.

As smartphones evolve into AI-powered personal computing hubs and wearables become more sophisticated, the importance of highly integrated, power-efficient, and AI-ready Mobile SoCs will only grow. Stakeholders who innovate in energy efficiency, AI capability, and manufacturing resilience will lead the way through 2032 and beyond.Read Full Report:-https://www.uniprismmarketresearch.com/verticals/semiconductor-electronics/mobile-soc

0 notes

Text

0 notes

Text

Online Form Builder: Simplify Data Collection with Ease

In the digital age, businesses and individuals need efficient ways to collect information, and an online form builder serves as the perfect solution. Whether for customer feedback, registrations, surveys, job applications, or lead generation, an online form builder allows users to create, customize, and share professional forms without requiring technical expertise. These tools eliminate the need for paper-based forms, streamlining data collection and enhancing overall productivity.

One of the biggest advantages of an online form builder is its user-friendly interface. Most form builders feature a drag-and-drop functionality, allowing users to design forms effortlessly. Users can add text fields, checkboxes, dropdown menus, and file upload options without writing a single line of code. This online form builder makes it easy for businesses, organizations, and even individuals to collect structured data efficiently.

Customization is another key feature of modern online form builders. Users can personalize forms by choosing from pre-designed templates or creating unique forms from scratch. These tools allow businesses to add logos, adjust colors, and customize fonts, ensuring that the forms align with their brand identity. Additionally, form builders support conditional logic, meaning that certain fields appear based on user responses, making forms more dynamic and interactive.

Seamless integration with other platforms is another major benefit. Popular online form builders integrate with CRM systems, email marketing tools, and payment processors like Google Sheets, HubSpot, Mailchimp, PayPal, and Stripe. This allows businesses to automatically store data, trigger automated workflows, and collect payments directly through forms. By reducing manual data entry, businesses save time and minimize errors.

Security and privacy are top concerns when collecting sensitive information online. The best online form builders come with SSL encryption, CAPTCHA verification, and GDPR compliance to protect user data. These features ensure that information is secure, preventing data breaches and unauthorized access. Businesses handling confidential data, such as medical forms or financial transactions, can trust these tools to maintain security standards.

Another significant advantage of online form builders is real-time data collection and analysis. Once a respondent submits a form, the data is instantly recorded and available for review. Businesses can track responses, generate reports, and analyze trends to make informed decisions. Some advanced form builders even offer built-in analytics, allowing users to visualize data through graphs and charts.

For businesses that rely on appointment scheduling or customer inquiries, online forms simplify the process. Instead of handling emails or phone calls manually, users can create booking forms where clients select available time slots and submit their details. This reduces administrative workload and improves customer experience.

Mobile responsiveness is another critical feature of modern online form builders. Since many users fill out forms using smartphones or tablets, the best form builders ensure that forms adapt to different screen sizes. This guarantees a smooth user experience, regardless of the device used.

Marketing professionals also benefit from online form builders by using them for lead generation and customer engagement. By embedding forms on websites, social media pages, or email campaigns, businesses can collect user information seamlessly. Forms with engaging CTAs (Call-to-Action) encourage visitors to subscribe to newsletters, sign up for webinars, or request a free consultation, helping businesses expand their customer base.

Automation is another powerful feature offered by online form builders. Users can set up automated email responses, follow-ups, and notifications based on form submissions. This ensures that respondents receive instant confirmation and further instructions if needed. Businesses save time by automating repetitive tasks, allowing them to focus on more strategic initiatives.

For industries that require signatures, electronic signature integration is a game-changer. Many form builders support e-signature fields, allowing users to sign contracts, agreements, or consent forms digitally. This eliminates the need for physical paperwork, speeding up processes and improving efficiency.

Educational institutions also leverage online form builders for managing student registrations, course enrollments, and feedback collection. Teachers and administrators can create custom forms that streamline school administration, making it easier to gather and manage data.

E-commerce businesses benefit from payment-enabled forms, where customers can place orders, select quantities, and make payments directly through the form. This simplifies checkout processes and enhances customer satisfaction.

Additionally, online form builders often support multi-step forms, which are useful for collecting detailed information without overwhelming users. Instead of presenting long and complex forms, users can progress through sections step by step, improving completion rates and user engagement.

To enhance accessibility, online form builders also support multiple languages, ensuring that businesses can reach a global audience. Whether creating surveys for international customers or managing multi-language registration forms, this online form bulilder feature allows seamless communication across different regions.

In conclusion, an online form builder is an essential tool for businesses, educators, marketers, and professionals who need a reliable way to collect and manage data. With features like drag-and-drop customization, real-time analytics, integrations, mobile responsiveness, automation, and security, these tools provide a seamless form-building experience. Whether used for lead generation, customer feedback, payments, or appointment scheduling, an online form builder simplifies workflows, improves efficiency, and enhances user experience.

0 notes

Text

Industrial Embedded Systems: The $118.1B Tech You Didn’t Know You Needed!

Industrial Embedded Systems Market is revolutionizing industries by integrating specialized computing systems into machinery and processes. These systems, comprising microcontrollers, processors, and software, enhance automation, efficiency, and reliability, supporting sectors like manufacturing, energy, automotive, and telecommunications. As digital transformation accelerates, embedded systems are unlocking new possibilities for smart and connected solutions.

To Request Sample Report : https://www.globalinsightservices.com/request-sample/?id=GIS33025 &utm_source=SnehaPatil&utm_medium=Article

📊 Market Growth & Key Insights

✅ Automotive leads, leveraging embedded systems for EVs, ADAS, and vehicle safety. ✅ Healthcare follows, driving advancements in medical diagnostics & smart devices. ✅ North America dominates, fueled by technological innovation and R&D investments. ✅ Europe ranks second, benefiting from IoT adoption and industrial automation. ✅ U.S. & Germany emerge as key players, supported by strong industrial ecosystems.

🔍 Market Segmentation & Trends

🔹 Type: Software, Hardware, Firmware 🔹 Technology: AI, IoT, Machine Learning, Edge Computing, Big Data 🔹 Application: Automotive (35%), Industrial Automation (30%), Consumer Electronics (25%) 🔹 Key Players: Intel, Texas Instruments, NXP Semiconductors

🚀 Future Outlook & Challenges

The future of industrial embedded systems is brighter than ever, with 5G integration, autonomous manufacturing, and AI-driven solutions driving growth. Regulatory standards like EU safety laws push companies toward continuous innovation. However, cybersecurity threats and high implementation costs pose challenges. With edge computing & IoT adoption surging, the market is set for massive expansion in smart factories & real-time analytics.

#industrialautomation #embeddedsystems #smartmanufacturing #iottech #aiintegration #industry40 #automotiveinnovation #5gtechnology #chiptechnology #electronicsengineering #robotics #bigdata #machinelearning #digitaltransformation #realtimedata #semiconductors #evtechnology #autonomoussystems #hardwareengineering #cloudcomputing #techtrends #processautomation #manufacturingtech #energytech #aerospaceengineering #industrialgrowth #automotivedesign #smartindustry #nextgencomputing #datasecurity #innovationtech #industrialiot #hightechsolutions #techindustry

Research Scope:

· Estimates and forecast the overall market size for the total market, across type, application, and region

· Detailed information and key takeaways on qualitative and quantitative trends, dynamics, business framework, competitive landscape, and company profiling

· Identify factors influencing market growth and challenges, opportunities, drivers, and restraints

· Identify factors that could limit company participation in identified international markets to help properly calibrate market share expectations and growth rates

· Trace and evaluate key development strategies like acquisitions, product launches, mergers, collaborations, business expansions, agreements, partnerships, and R&D activities

About Us:

Global Insight Services (GIS) is a leading multi-industry market research firm headquartered in Delaware, US. We are committed to providing our clients with highest quality data, analysis, and tools to meet all their market research needs. With GIS, you can be assured of the quality of the deliverables, robust & transparent research methodology, and superior service.

Contact Us:

Global Insight Services LLC 16192, Coastal Highway, Lewes DE 19958 E-mail: [email protected] Phone: +1–833–761–1700 Website: https://www.globalinsightservices.com/

0 notes

Text

The Future of White Box Servers: Market Outlook, Growth Trends, and Forecasts

The global white box server market size is estimated to reach USD 44.81 billion by 2030, according to a new study by Grand View Research, Inc., progressing at a CAGR of 16.2% during the forecast period. Increasing adoption of open source platforms such as Open Compute Project and Project Scorpio coupled with surging demand for micro-servers and containerization of data centers is expected to stoke the growth of the market. Spiraling demand for low-cost servers, higher uptime, and a high degree of customization and flexibility in hardware design are likely to propel the market over the forecast period.

A white box server can be considered as a customized server built either by assembling commercial off-the-shelf components or unbranded products supplied by Original Design Manufacturers (ODM) such as Supermicro; Quanta Computers; Inventec; and Hon Hai Precision Industry Company Inc. These servers are easier to design for custom business requirements and can offer improved functionality at a relatively cheaper cost, meeting an organization’s operational needs.

Evolving business needs of major cloud service and digital platform providers such as AWS, Google, Microsoft Azure, and Facebook are leading to increased adoption of white box servers. Low cost, varying levels of flexibility in server design, ease of deployment, and increasing need for server virtualization are poised to stir up the adoption of white box servers among enterprises.

Data Analytics and cloud adoption with increased server applications for processing workloads aided by cross-platform support in a distributed environment is also projected to augment the market. Open Infrastructure conducive to software-defined operations and housing servers, storage, and networking products will accentuate the market for storage and networking products during the forecast period.

Additionally, ODMs are focused on price reduction as well as innovating new energy-efficient products and improved storage solutions, which in turn will benefit the market during the forecast period. However, ODM’s limited service and support services, unreliable server lifespans, and lack of technical expertise to design and deploy white box servers can hinder market growth over the forecast period.

White Box Server Market Report Highlights

North America held the highest market share in 2023. The growth of the market can be attributed to the high saturation of data centers and surging demand for more data centers to support new big data, IoT, and cloud services

Asia Pacific is anticipated to witness the highest growth during the forecast period due to the burgeoning adoption of mobile and cloud services. Presence of key manufacturers offering low-cost products will bolster the growth of the regional market

The data center segment is estimated to dominate the white box server market throughout the forecast period owing to the rising need for computational power to support mobile, cloud, and data-intensive business applications

X86 servers held the largest market revenue share in 2023. Initiatives such as the open compute project encourage the adoption of open platforms that work with white box servers

Curious about the White Box Server Market? Get a FREE sample copy of the full report and gain valuable insights.

White Box Server Market Segmentation

Grand View Research has segmented the global white box server market on the basis of type, processor, operating system, application, and region:

White Box Server Type Outlook (Revenue, USD Million, 2018 - 2030)

Rackmount

GPU Servers

Workstations

Embedded

Blade Servers

White Box Server Processor Outlook (Revenue, USD Million, 2018 - 2030)

X86 servers

Non-X86 servers

White Box Server Operating System Outlook (Revenue, USD Million, 2018 - 2030)

Linux

Windows

UNIX

Others

White Box Server Application Outlook (Revenue, USD Million, 2018 - 2030)

Enterprise Customs

Data Center

White Box Server Regional Outlook (Revenue, USD Million, 2018 - 2030)

North America

US

Canada

Mexico

Europe

UK

Germany

France

Asia Pacific

China

India

Japan

Australia

South Korea

Latin America

Brazil

Middle East and Africa (MEA)

UAE

Saudi Arabia

South Africa

Key Players in the White Box Server Market

Super Micro Computer, Inc.

Quanta Computer lnc.

Equus Computer Systems

Inventec

SMART Global Holdings, Inc.

Advantech Co., Ltd.

Radisys Corporation

hyve solutions

Celestica Inc.

South Korea

Latin America

Brazil

Middle East and Africa (MEA)

UAE

Saudi Arabia

South Africa

Order a free sample PDF of the White Box Server Market Intelligence Study, published by Grand View Research.

0 notes

Text

Automotive Hypervisor Market To Witness the Highest Growth Globally in Coming Years

The report begins with an overview of the Automotive Hypervisor Market 2025 Size and presents throughout its development. It provides a comprehensive analysis of all regional and key player segments providing closer insights into current market conditions and future market opportunities, along with drivers, trend segments, consumer behavior, price factors, and market performance and estimates. Forecast market information, SWOT analysis, Automotive Hypervisor Market scenario, and feasibility study are the important aspects analyzed in this report.

The Automotive Hypervisor Market is experiencing robust growth driven by the expanding globally. The Automotive Hypervisor Market is poised for substantial growth as manufacturers across various industries embrace automation to enhance productivity, quality, and agility in their production processes. Automotive Hypervisor Market leverage robotics, machine vision, and advanced control technologies to streamline assembly tasks, reduce labor costs, and minimize errors. With increasing demand for customized products, shorter product lifecycles, and labor shortages, there is a growing need for flexible and scalable automation solutions. As technology advances and automation becomes more accessible, the adoption of automated assembly systems is expected to accelerate, driving market growth and innovation in manufacturing.

The global automotive hypervisor market size was USD 137.1 million in 2020. The market is projected to grow from USD 158.1 million in 2021 to USD 1,475.7 million in 2028 at a CAGR of 37.6% during the 2021-2028 period.

Get Sample PDF Report: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/106411

Key Strategies

Key strategies in the Automotive Hypervisor Market revolve around optimizing production efficiency, quality, and flexibility. Integration of advanced robotics and machine vision technologies streamlines assembly processes, reducing cycle times and error rates. Customization options cater to diverse product requirements and manufacturing environments, ensuring solution scalability and adaptability. Collaboration with industry partners and automation experts fosters innovation and addresses evolving customer needs and market trends. Moreover, investment in employee training and skill development facilitates seamless integration and operation of Automotive Hypervisor Market. By prioritizing these strategies, manufacturers can enhance competitiveness, accelerate time-to-market, and drive sustainable growth in the Automotive Hypervisor Market.

Major Automotive Hypervisor Market Manufacturers covered in the market report include:

Siemens AG (Munich, Germany) Green Hills Software (California, U.S.) Windriver System (Alameda, U.S.) BlackBerry Ltd (Waterloo, Canada) Renesas Electronic Corporation (Tokyo, Japan) Sasken (Bangalore, India) Continental (Hanover, Germany) Harman (Stamford, U.S.) Hangsheng Technology GmbH (Berlin, Germany) IBM Corporation (New York, U.S)

operating players are more focusing on virtualization in many ways to reduce these complexities in future vehicles. Moreover, embedded virtualization technology allows processors a unique resource to multiple applications and OS in a secure/safe manner.

Trends Analysis

The Automotive Hypervisor Market is experiencing rapid expansion fueled by the manufacturing industry's pursuit of efficiency and productivity gains. Key trends include the adoption of collaborative robotics and advanced automation technologies to streamline assembly processes and reduce labor costs. With the rise of Industry 4.0 initiatives, manufacturers are investing in flexible and scalable Automotive Hypervisor Market capable of handling diverse product portfolios. Moreover, advancements in machine vision and AI-driven quality control are enhancing production throughput and ensuring product consistency. The emphasis on sustainability and lean manufacturing principles is driving innovation in energy-efficient and eco-friendly Automotive Hypervisor Market Solutions.

Regions Included in this Automotive Hypervisor Market Report are as follows:

North America [U.S., Canada, Mexico]

Europe [Germany, UK, France, Italy, Rest of Europe]

Asia-Pacific [China, India, Japan, South Korea, Southeast Asia, Australia, Rest of Asia Pacific]

South America [Brazil, Argentina, Rest of Latin America]

Middle East & Africa [GCC, North Africa, South Africa, Rest of the Middle East and Africa]

Significant Features that are under offering and key highlights of the reports:

- Detailed overview of the Automotive Hypervisor Market.

- Changing the Automotive Hypervisor Market dynamics of the industry.

- In-depth market segmentation by Type, Application, etc.

- Historical, current, and projected Automotive Hypervisor Market size in terms of volume and value.

- Recent industry trends and developments.

- Competitive landscape of the Automotive Hypervisor Market.

- Strategies of key players and product offerings.

- Potential and niche segments/regions exhibiting promising growth.

Frequently Asked Questions (FAQs):

► What is the current market scenario?

► What was the historical demand scenario, and forecast outlook from 2025 to 2032?

► What are the key market dynamics influencing growth in the Global Automotive Hypervisor Market?

► Who are the prominent players in the Global Automotive Hypervisor Market?

► What is the consumer perspective in the Global Automotive Hypervisor Market?

► What are the key demand-side and supply-side trends in the Global Automotive Hypervisor Market?

► What are the largest and the fastest-growing geographies?

► Which segment dominated and which segment is expected to grow fastest?

► What was the COVID-19 impact on the Global Automotive Hypervisor Market?

Table Of Contents:

1 Market Overview

1.1 Automotive Hypervisor Market Introduction

1.2 Market Analysis by Type

1.3 Market Analysis by Applications

1.4 Market Analysis by Regions

1.4.1 North America (United States, Canada and Mexico)

1.4.1.1 United States Market States and Outlook

1.4.1.2 Canada Market States and Outlook

1.4.1.3 Mexico Market States and Outlook

1.4.2 Europe (Germany, France, UK, Russia and Italy)

1.4.2.1 Germany Market States and Outlook

1.4.2.2 France Market States and Outlook

1.4.2.3 UK Market States and Outlook

1.4.2.4 Russia Market States and Outlook

1.4.2.5 Italy Market States and Outlook

1.4.3 Asia-Pacific (China, Japan, Korea, India and Southeast Asia)

1.4.3.1 China Market States and Outlook

1.4.3.2 Japan Market States and Outlook

1.4.3.3 Korea Market States and Outlook

1.4.3.4 India Market States and Outlook

1.4.3.5 Southeast Asia Market States and Outlook

1.4.4 South America, Middle East and Africa

1.4.4.1 Brazil Market States and Outlook

1.4.4.2 Egypt Market States and Outlook

1.4.4.3 Saudi Arabia Market States and Outlook

1.4.4.4 South Africa Market States and Outlook

1.5 Market Dynamics

1.5.1 Market Opportunities

1.5.2 Market Risk

1.5.3 Market Driving Force

2 Manufacturers Profiles

Continued…

About Us:

Fortune Business Insights™ delivers accurate data and innovative corporate analysis, helping organizations of all sizes make appropriate decisions. We tailor novel solutions for our clients, assisting them to address various challenges distinct to their businesses. Our aim is to empower them with holistic market intelligence, providing a granular overview of the market they are operating in.

Contact Us:

Fortune Business Insights™ Pvt. Ltd.

US:+18339092966

UK: +448085020280

APAC: +91 744 740 1245

0 notes

Text

Europe Automotive Camera Market Trends, Size, Share, Growth, Analysis, Forecast to 2028

The automotive camera market in Europe is expected to grow from US$ 2,414.23 million in 2022 to US$ 8,439.24 million by 2028; it is estimated to grow at a CAGR of 23.2% from 2022 to 2028.

The Europe automotive camera market growth is attributable to the rising adoption of advanced cameras in vehicles. The automotive cameras assist the driver in parking, maneuvering, and assessing the vehicle's performance. The camera systems have played a crucial role in a few recent applications, including Lane Departure Warning Systems (LWDS), Forward Collision Warning System (FCWS), and Blind Spot Warning (BSW). In light and heavy commercial vehicles, the adoption of automotive cameras is growing in various system solutions, such as rear view camera, surround view camera, e-mirror, and driver monitoring systems (DMS). The cameras can be embedded with advanced computer vision algorithms for real machine vision systems for the advanced driver assistance systems (ADAS). Thus, the increase in applications of cameras in automotive vehicles and the rise in technological advancements fuel the adoption of advanced cameras in cars.

📚 𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐒𝐚𝐦𝐩𝐥𝐞 𝐏𝐃𝐅 𝐂𝐨𝐩𝐲 https://www.businessmarketinsights.com/sample/BMIRE00026047

The leading players providing automotive cameras are significantly adopting advanced technologies. For instance, in May 2021, StradVision, a leading company in AI-based vision processing technology for autonomous vehicles and automotive ADAS, introduced the latest features of camera perception software named “SVNet”. It is a deep learning-based perception software that supports ADAS features, including highway driving assist and automated valet parking. In addition, the rear view camera provided by STMicroelectronics for automotive vehicles caters to various applications, such as state-of-the-art HDR image sensors VG6640 and a versatile image signal processor (ISP) that offers excellent flicker-free image quality at HD resolution.

𝐓𝐡𝐞 𝐋𝐢𝐬𝐭 𝐨𝐟 𝐂𝐨𝐦𝐩𝐚𝐧𝐢𝐞𝐬

Aptiv PLC

Autoliv Inc.

Continental AG

FLIR Systems, Inc.

Gentex Corporation

Magna International Inc.

Mobileye

Robert Bosch GmbH

Stonkam Co., Ltd.

Valeo

📚𝐅𝐮𝐥𝐥 𝐑𝐞𝐩𝐨𝐫𝐭 𝐋𝐢𝐧𝐤 @ https://www.businessmarketinsights.com/reports/europe-automotive-camera-market

It also provides its product offerings for Driver Monitoring System (DMS) applications, through its HDR Europe Shutter sensor (1.6 Mpixel and 2.3 Mpixel), along with a multichannel voltage regulator and automotive-led drivers, MEMS sensors, ensuring greater flexibility for high-end computer vision applications in critical weather conditions and environments. Thus, the rising adoption of advanced cameras bolsters the automotive camera market growth

Segments Covered By Application

Park Assist

ADAS

By Type

Mono Camera

Surround View Camera

Rear View Camera

By Vehicle Type

Passenger Cars

Commercial Vehicle

By Level of Autonomy

L1

L2

L3

Europe Automotive Camera Regional Insights

The geographic scope of the Europe Automotive Camera refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

The European Automotive Camera Market: Trends, Growth, and Future Outlook

The automotive industry is rapidly evolving, with technological advancements playing a central role in shaping its future. Among these innovations, automotive cameras have become indispensable in modern vehicles. The European automotive camera market, in particular, has seen significant growth in recent years, driven by a variety of factors including consumer demand for enhanced safety, regulatory requirements, and the global push towards autonomous driving.

Market Overview

The European automotive camera market is a crucial component of the larger automotive technology sector. Automotive cameras are integrated into vehicles for a wide range of functions, such as Advanced Driver Assistance Systems (ADAS), autonomous driving, parking assistance, and surveillance. The demand for automotive cameras in Europe has been rising steadily due to increasing awareness of road safety, tighter safety regulations, and advancements in vehicle automation technologies.

In 2024, the European automotive camera market is projected to continue its upward trajectory, with growth driven by the ongoing shift towards electric and autonomous vehicles. The growing adoption of these vehicles in the region is expected to expand the demand for high-quality camera systems, which play a vital role in both safety and functionality.

𝐀𝐛𝐨𝐮𝐭 𝐔𝐬:

Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications.

You can see this-

Europe Bottled Water Market- https://www.globalpostnews.com/uncategorized/europe-bottled-water-market-by-key-players-regional-segmentation-and-forecasts-2023-2028/

North America Multi-Cloud Management Market- https://www.tumblr.com/nerdycreationdetective/776988758290710528/north-america-multi-cloud-management-market-size

0 notes

Text

🦾 Next-Gen Prosthetics: How Semiconductors Are Powering Bionic Breakthroughs!

Semiconductor-Based Smart Prosthetics Market : The fusion of semiconductor technology and biomedical engineering is driving groundbreaking advancements in smart prosthetics, offering enhanced mobility, sensory feedback, and real-time adaptability for individuals with limb loss. With AI-powered microchips, neuromuscular interfaces, and energy-efficient sensors, semiconductor-based prosthetics are transforming the future of bionic limbs and assistive devices.

To Request Sample Report : https://www.globalinsightservices.com/request-sample/?id=GIS32987 &utm_source=SnehaPatil&utm_medium=Linkedin

How Semiconductor Technology Powers Smart Prosthetics

Modern prosthetics leverage high-performance semiconductors to create responsive, intuitive, and adaptive solutions. Key innovations include: